PSD2 for your Ecommerce

PSD2 for your Ecommerce

Do you have an Ecommerce? From September the 14th 2019, the new PSD2 (Payment Services Directive 2) European directive for digital payments becomes effective.

Do you receive payments with a credit card?

If you own an ecommerce and receive payments through credit cards, you should read our article to know what’s going to change in the digital payments world.

PSD2: more safety for online shopping

What are the goals of this new European directive?

To implement better safety for online shopping and e-commerce owners; Align online shops on innovative transactions; To increase user’s safety and data protection; to encourage Open Banking, a new financial model based on authorized data sharing with different subject in the banking eco-system.

For e-commerce owners, this new initiative grants increased safety for online trade and compliance with the current standards. Each consumer can now pay or access personal banking information without being concerned about fraud or privacy violation.

PSD2 for your Ecommerce

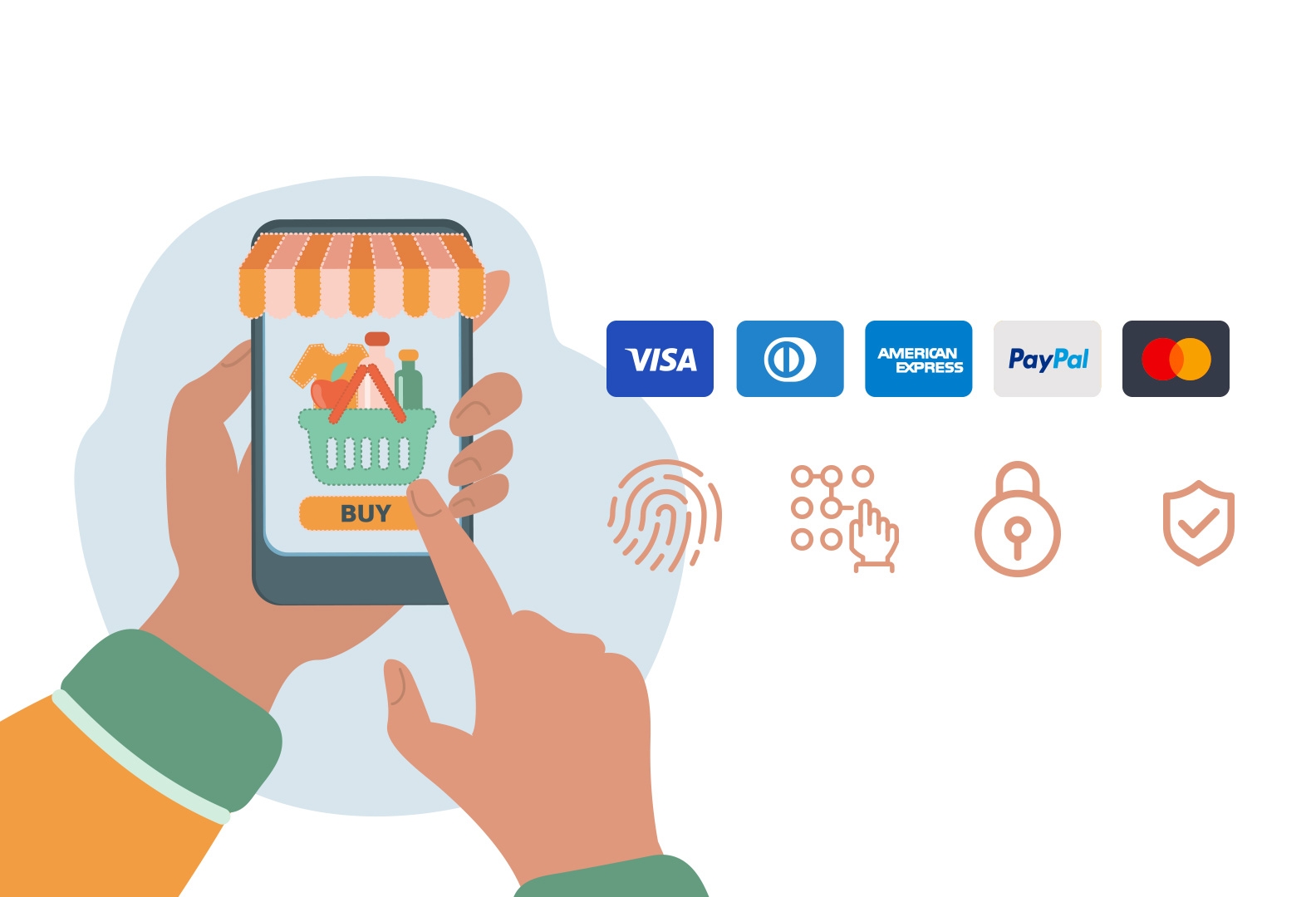

What’s SCA?

PSD2 overlaps currently operative directives and sets different rules for users and providers which offer digital payment services, like PayPal, Nexi Cartasi, Unicredit, Bancasella, Stripe, Braintree.

One of the biggest news in the implementation of the SCA (Strong Customer Authentication), a mechanism that requires a two-factor authentication from online buyers.

PSD2 for your Ecommerce

What’s going to change when paying online?

At this time, who buys online can use a credit card with its related security number.

If using PayPal, the only requested information is a standard password.

On the other hand, according to the new directive, the buyers will need to prove their identity through a two-factor authentication.

The two identification factors can be chosen among the following:

PIN or Password. Smartphone or a device which has been previously identified by the bank (this comes with a safety number). A physical recognition system, such as fingerprints, face, or voice.

PSD2 for your Ecommerce

Exceptions to the directive

PSD2 for your Ecommerce. The new framework only covers online payments, which are not already guarded by a high-level security methods.

Excluded methods:

Direct charge

Invoice

Prepayments

Sums lower than 30 euros

How will SCA impact on your online shop?

The main difference rests in the payment procedure, which now includes a second authentication factor.

With PayPal, the second auth factor will be automatically added to the payment process, so no action is required.

For other payment platforms, an adjustment is needed.

I.e., on Stripe and Braintree, you need to implement new elements in the check-out phase, to be compliant.

If you are using an open-source platform like PrestaShop, WooCommerce, or Magento, and you operate with payment plug-ins, you would probably need to update them.

In any case, these operations should be performed by a technician.

SCA against e-commerce frauds

The cost of online scams with credit cards is around 1.3 Billion each year, in Europe only.

SCA requires a second step in the authentication process for online payments, making it much harder for scammers to use stolen credit card numbers, passwords, or log-in data.

The e-commerce sector is international: for that, it has been necessary to implement this directive at a European level, to protect buyers and e-commerce owners.

What will improve?

We expect that PSD2 will make improvements for consumers and e-commerce owners.

There are many opportunities for the ones able to manage this change, and we want to enlight five of them:

Open Banking: creation of an open banking system

New online payment tools: the directive introduces two new authentication systems, SCA and 3DS 2.0, which allow to improve online transactions safety against the risk of fraud for consumers.

Improved customer’s online experience: thanks to the information-sharing among authorized third-parties. Merchants and online stores will be able to implement complete payment procedures within their web pages, offering an efficient and broker-free service.

Cost reduction for customers: inter-bank fees for credit card payments will be reduced.